Terakhir diperbarui: 02-03-2026, 06:28

S&P Warned Rising Fiscal Pressures Could Weigh on Indonesia's BBB Rating

S&P Global Ratings warned that rising fiscal pressures, particularly higher debt-servicing costs, are increasing downside risks to Indonesia's sovereign credit profile and could trigger negative rating action, noting interest payments likely exceeded 15% of govt. revenue in 2025 and may warrant a more negative view if sustained. While S&P maintained Indonesia's BBB rating with stable outlook, it flagged risks to fiscal buffers amid revenue weakness, following Moody's earlier revision of outlook to negative from stable on Baa2 rating, citing governance and fiscal concerns. The warnings, alongside calls for market reforms, added pressure to already fragile foreign investor sentiment despite govt. assurances of ongoing reforms and improving economic momentum. (Bloomberg)

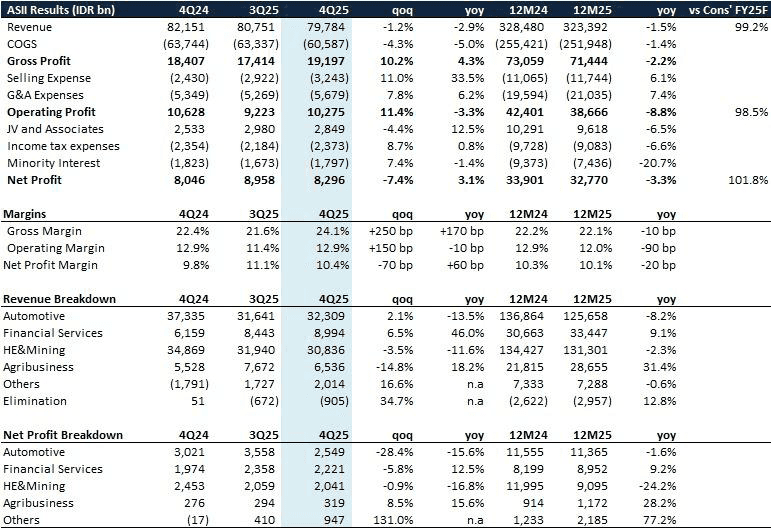

BCAS: ASII IJ - 4Q25 Results: inline with consensus estimate

- ASII 12M25 Results was inline with consensus estimate with revenue and net profit reached 99.2% and 101.8%, respectively.

- 2025 net profit was -3.3% yoy, Auto segment -1.6% yoy due to weak domestic 4W sales and HE&Mining dropped 24% yoy.

- 2025 Revenue slightly declined 1.5 yoy; while operating profit dropped deeper -8.8%.

- Astra proposes a final dividend of IDR 292/sh (4.3% yield), that form final dividend of IDR 390/sh (included IDR98/sh interim dividend), representing payout ratio of 48%

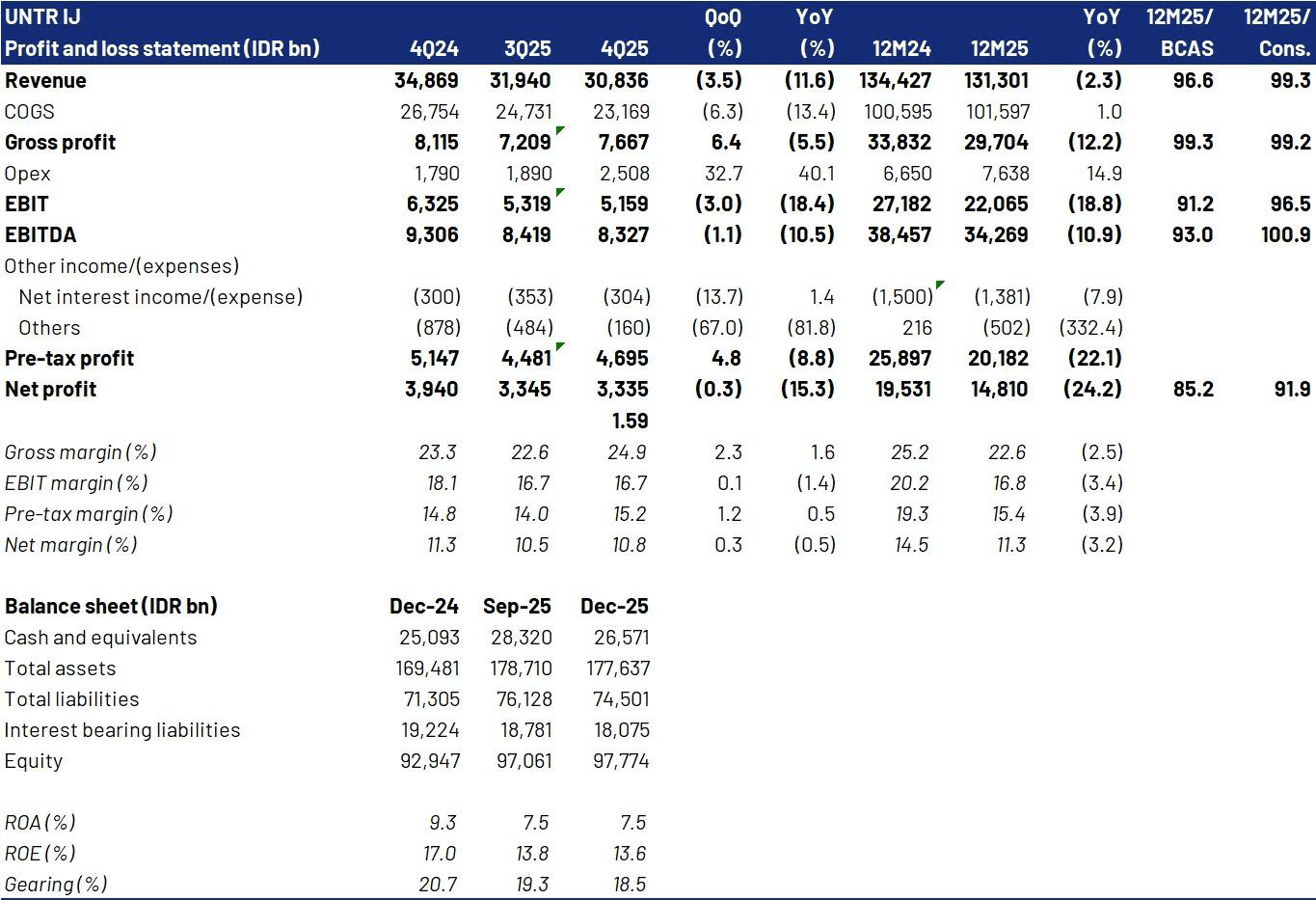

BCAS: UNTR IJ - 4Q25 - Hit by Lower Activities and Unexpected Opex, Below Expectations at 85.2% of Ours and 91.9% of Street

- UNTR's 4Q25 revenue fell to IDR 30.8 tn (-3.5% QoQ, -11.6% YoY), on the back of lower contribution from heavy equipment sales at 862 units (-6.8% QoQ, -21.6% YoY), coupled with weakening mining activities, which impacted OB removal, declining 7.3% QoQ and 8.2% YoY to 273 Mbcm. This brought FY25 revenue down to IDR 131.3 tn (-2.3% YoY), far below our projection (83.4%) and the Street (91.9%).

- At the gross profit level, efficiency improvements in operations successfully increased overall margin, with GPM rising to 24.9% (+230 bps QoQ, +160 bps YoY). However, due to a spike in opex driven by higher impairment provisions of IDR 587 bn (4Q24: IDR 39 bn), total opex surged to IDR 2.5 tn (+32.7% QoQ, +40.1% YoY), which pressured EBIT down to IDR 5.2 tn (-3.0% QoQ, -18.4% YoY) despite operational improvement. Consequently, FY25 EBIT declined to IDR 22.1 tn (-18.8% YoY), below our estimate (91.2%) and the Street (100.9%).

- Moreover, losses from impairment related to the Company's JV in Supreme Energy Rantau Dedap dragged net profit down to IDR 3.3 tn (-0.3% QoQ, -15.3% YoY). As a result, FY25 net profit fell to IDR 14.8 tn (-24.2% YoY), far below our forecast at 85.2% and the Street at 91.9%.

Garuda Indonesia (GIAA) Used IDR 23.7 Tn Injection from Danantara to Settle Avtur and Maintenance Arrears

GIAA has used a capital injection of IDR 23.7 tn from Danantara to fully settle outstanding arrears for avtur fuel and aircraft maintenance, improving its cash flow and operational stability as part of broader restructuring and turnaround efforts. The settlement removes significant past dues that had constrained operations, supporting GIAA's path toward more sustainable financial and operational footing. (Bisnis.com)